Over the past 30 years we have borne witness to the collapse of the private pension system with for-profit employers, tax-exempt entities and now the governmental sector replacing defined benefit pension programs (DB) with defined contribution plans (DC)1. This evolution has represented one well-documented transfer of risk: the transfer of investment risk and its related funding risk from employers to employees. However, this risk transfer did not come without a cost to employers.

Defined contribution plans make the participant the sole decision maker for the four factors that determine an employee’s ability to retire successfully: contribution rate, investment strategy/return, time horizon, and spending needs in retirement.

Retirement Preparation in a Defined Contribution World

In the transition from DB to DC, these critical elements were transitioned from sophisticated pension committees and diligent plan sponsors, to participants that in many cases lack the expertise, tools, or time to manage them effectively.

While the transition from DB to DC has fulfilled the promise of offloading the funding risk from plan sponsors to participants, it has created a number of unintended consequences that create challenges in trying to meet the objective of retirement security for employees. In particular, the DB pension model is particularly successful in pooling longevity risk to ensure that participants do not run out of income in retirement. In the DB model, some participants would die at younger ages and therefore receive fewer payments from the plan, while some participants would live longer and receive greater benefits than "average."

DC plans are fundamentally different in so much as each participant has to account for their own longevity risk. Because each participant is on their own, there is no ability to average out the risk of outliving your income and each participant needs to plan for the likelihood they might exceed the average. In 2010, the Social Security Administration reported US life expectancy at 78. However, a male who reaches normal retirement age as measured by Social Security lives on average until age 84. Average life expectancy is just that, average; plan participants must plan and save to live well into their 90s. As a result, while transferring the risk to participants, DC plans push the goal line farther away for participants. Each participant is faced with the daunting task of managing a pension plan for one and the results are startling:

Employees whose primary retirement plan is a defined contribution plan tend to retire one to two years later than employees covered by a pension plan2

Individuals covered only by a defined benefit plan are 87% more likely to retire in any given year than individuals only covered by a defined contribution plan3

A 1% increase in the S&P 500 Index in any given year increases the probability that the pre-retiree will retire by 2.5%4

Delayed retirements may also increase employers’ healthcare costs. Healthcare costs for a 65-year-old worker are twice those of a worker between 45 and 545

The ability to retain young talent is impacted by the prospect of career and professional advancement

At the same time when participants are adjusting to managing their own retirement, research has shown that people are hard-wired with behavioral biases that make them ill-equipped to make the prudent, rationale choices everyone assumes.

Behavioral Challenges to the DC Model

Retirement Readiness

For the DC plan system to survive, employers must revisit the purpose of the plan. While the DC model began as a supplementary tool for participants with pension benefits, they have transitioned into the primary retirement savings vehicles for millions of participants. Along the way, the ancillary benefits of giving employees flexibility, choice, and access have become the tail wagging the dog of the retirement plan with little thought given to the end goal of a successful retirement.

Returning to the primary purpose of providing retirement benefits will require sponsors, and the vendors they hire, to communicate with participants in a manner that allows a participant to reasonably estimate how the factors within their control – contribution rate, investment choices, time horizon, and spending needs – impact their retirement success. This transition in communication model we broadly refer to as "retirement readiness."

The concept of retirement readiness is predicated on the practice of taking current assets and assumptions about future behavior to make estimates as to the level of income a participant could reasonably expect to receive in retirement. The big change that comes with the retirement readiness concept is in changing the focus to income rather than assets. The best retirement programs focus communications with participants on income rather than assets. While assets will change with the rise and fall of markets, retirement income expectations are substantially less market dependent. With this shift, participants are left to focus on the things within their control to improve their retirement savings program.

Calculating and reporting retirement income estimates is the participant-equivalent of the funding levels that pension plans calculate and report. As we transition the responsibility for managing retirement success to participants the only reasonable way to approach the challenge is to provide participants with the tools to understand their own "funding status."

Unfortunately, merely reporting replacement income for participants will not magically fix the DC system overnight. Sponsors who wish to drive the best outcomes for participants may need to reexamine historical decisions that continue to impact the design of their plan.

LIFECYCLE OF A DEFINED CONTRIBUTION PLAN

With the wealth of data availability about participants, there is a tendency to use data to obscure what is otherwise a simple math problem. What is the rate of savings by wage, age, and sex? Does the sales staff save more or less than the IT staff? While these data points are interesting, they continue the fallacy that a magic education session focused on 35 year old men earning between $30,000 and $40,000 a year will change the way they have made, and will continue to make, decisions on how to best utilize the retirement plan.

Within the DC plan we think it is wise to look at participants in three groups:

Young Savers – This group is in the early stages of their retirement savings process; they generally have lower incomes and more competing priorities for income that can be allocated to savings.

Accumulators – This group is generally mid-career and is highly productive within the organization. In many cases they have progressed to a level of financial security and as a result are more able to think about retirement

Pre-Retirees – Most pre-retirees have concluded the costs of developing and supporting a family and have tremendous experience within the organization. Saving for retirement may be their primary financial "goal."

Plan sponsors should increasingly be looking at the four factors within their control: plan design, plan services, investment structures, and employee education, to maximize the efficacy of their retirement plan, thereby improving the health and satisfaction of their employee population.

PLAN DESIGN

In any retirement plan, design is the primary determinant of a plan’s effectiveness. Unfortunately, many employers focus nearly exclusively on the rate and methodology of the employer contribution, neglecting other factors that have an equivalent impact. Plan sponsors should evaluate the design of their plan with the lens focused on how the design impacts their three population groups.

Young Savers

Most studies support that an employee must save, or have contributed on their own behalf, 10 – 15% of their income over a working career. Each year that a participant fails to save, or fails to save at an acceptable rate, increases the amount they must save in the future. Accordingly, an effective plan focuses on quickly getting participants to a sustainable target retirement savings rate.

In trying to get Young Savers started on the path to retirement success, there are three tools that can materially drive improvements in participant behavior: Automatic Enrollment, Automatic Escalation, and Hybrid Match Formulas.

Automatic Enrollment is a simple process that switches the "default" behavior for participants who fail to make an election. Rather than the default decision being a participant is not enrolled in the plan, under an automatic enrollment program the default action is to enroll participants at a pre-defined deferral percentage. According to a 2013 study from Fidelity, 22% of corporate retirement plans utilize an automatic enrollment feature. For sponsors not implementing automatic enrollment, the primary objection has to do with how effective the feature is, and the resultant increase in match costs it might incur for the employers who utilize it. That objection demonstrates the effectiveness of the provision in changing participant behavior.

According to the same Fidelity study, the plan participation rate for plans not utilizing automatic enrollment averages 54% versus 83% for plans with automatic enrollment. The tremendous differences in plan participation rates are a meaningful step in improving prospective participant retirement readiness. Some plan sponsors are taking automatic enrollment a step further by developing annual automatic re-enrollment programs that require an employee who does not wish to participate to opt-out each year. Surprisingly, the rates of participation for plans that re-enroll all existing employees are not materially lower than plans that implement an automatic enrollment feature only prospectively.

Most automatic enrollment features have a pre-defined deferral rate of 3-5% of pay. Empirically, the rate that the plan sponsor selects has very little impact on opt-out rates. Unfortunately, even for plans that automatically enroll at 5% of pay, employer contributions may not be sufficient to deliver adequate retirement income. To address this challenge, sponsors are frequently marrying automatic enrollment with an automatic escalation feature to the plan. Under automatic escalation, participants have their deferral rate increased (typically by 1%) annually until the deferral rate hits a level specified by the employer.

To provide an example, a plan that matches of 100% of the first 5% an employee defers may have an automatic enrollment feature of 5%. The deferral plus the match would generate a retirement savings of 10%. If the sponsor has determined that 15% is generally necessary to provide an adequate retirement, they may elect an automatic increase program that increases the default deferral rate from 5% initially until the participant achieves the desired 10% deferral rate.

As with an automatic enrollment feature, automatic escalation is not dictatorial and an employee can opt-out of participation or increases at any time. While participants can opt-out if desired, many participants find the automatic nature of these programs to be beneficial into changing their behavior.

Data is mixed as to the impact that an employer contribution has on plan participation and deferral rates. However, plans that provide a portion of their employer benefit as a match do ellicit a specific type of deferral behavior based on the match rate. As in my earlier example, a plan that matches 100% of the first 5% an employee defers will find that many of their participants enroll at the 5% level, with or without automatic enrollment. Developing employer contribution formulas that reinforce the automatic enrollment program maintain a consistent voice to participants that the employer is concerned with retirement readiness and has designed their plan accordingly.

While historically many plan sponsors chose either non-elective contributions or a match contribution exclusively, many plan sponsors are electing hybrid contribution formulas. The hybrid approach provides a benefit for all employees regardless of whether they elect to participate and a match contribution to incent the required savings behaviors.

To provide another example, a sponsor that might currently have a plan that matches 100% of the first 5% an employee defers may instead consider a 2% contribution for all employees, and a match of 30% of the first 10% an employee defers. The funding cost to the employer would be the same but a participant that provides the full 10% deferral contribution would receive the 5% employer contribution and the target 15% savings rate is met.

Accumulators

While Young Savers need to be incented to get into the program, Accumulators are more likely to have already started accumulating retirement assets. For these employees, the biggest challenge is with staying the course and not getting sidetracked by shorter-term goals. The easiest way to get sidetracked is during employment transitions. Many Accumulators have started and stopped saving multiple times. According the Bureau of Labor Statistics, in 2012 the average 35 – 46 year old held 2.1 jobs6, meaning many participants will have a separation of service during some of their prime accumulation years. With each separation of service employees have a decision to make with respect to their retirement savings.

The Government Accountability Office (GAO)7 reports that only 20% of employees who take a lump-sum distribution roll proceeds into a tax-qualified IRA or retirement plan account. From a design perspective, sponsors have no control over what participants do with retirement assets accumulated at previous employers, but providing within your plan the ability to accept rollovers from other employers, at a minimum provides a new employee the easy option of keeping money in the retirement system. As recently as March 7, 2013 the GAO issued their report entitled Labor and IRS Could Improve the Rollover Process for Participants, which recommended that the DOL and IRS take certain steps to reduce obstacles and disincentives to plan-to-plan rollovers.

Another source of retirement leakage are plan loans. Retirement plan loans have unfortunately become a frequently added feature to most DC plans. Retirement plan loans provide quick, and in most cases, low cost access to capital for employees who want it. Most participant loan interest rates are tied to the Prime Interest Rate, but the evidence is that retirement plan borrowers are anything but "Prime."

Navigant Economics estimated the loan default rate from July 2011 – May 2012 was 17.4%. Simultaneously, the percentage of active participants with a loan outstanding has reached its highest historical level, 18.5%.

At the current rate of progress, nearly $1 trillion in retirement accumulations will be participant IOUs. Undoubtedly participants appreciate loan features when they feel they need access to cash, although the argument that participants need the option for loans to weather economic crisis is muted by the fact that the biggest economic crisis most employees may face is unemployment, for which loans do not provide any solution. Additionally, there is no academic evidence to support that a plan loan feature increases either participation rates or deferral rates, but the evidence to support that loan features hurt broad retirement readiness is inescapable.

Pre-Retirees

For many organizations the anticipated generational transition of the workforce is necessary for the health and vitality of an organization. Retirement uncertainty is a significant deterrent to this type of turnover. From a plan design perspective, many plan sponsors have implemented a plan feature that is designed to please participants but may not be in participants’ best interests. Similar to loan features, many plan sponsors have imbedded in-service plan distribution provisions that provide participants at a specified age, commonly 59 ½, the freedom to begin taking distributions while they continue to work.

The in-service distribution pleases participants because it provides greater freedom and access to their funds. However, allowing employees to take distributions while they are employed and continue to receive compensation and benefits fails on two fronts. For participants, in-service distributions by their very nature are not funding retirement expenses. For employers, in-service distributions do not encourage the generational transition that employers may desire.

If allowed, in-service distribution features should be carefully examined and ideally tied to a strategic phased retirement program that specifies a certain retirement date. Failure to implement this kind of control allows participants to simultaneously enjoy all the certainty and benefits of employment with the additional financial resources of accumulated retirement accounts. In-service distributions are frequently used to augment a participant’s standard of living rather than supplying retirement income, and feeds the human preference for pleasure today at the expense of retirement security in the future.

Plan Design Summary

If plan sponsors evaluate their plan design with a focus on the needs of their Young Savers, Accumulators, and Pre-Retirees, they may find opportunity to make changes that improve the likelihood of a successful retirement for all three groups. Importantly, the design choices discussed above do not require preference for one group over another, and while they may be targeted for each group specifically, there would be ancillary benefits to the other groups as well.

PLAN SERVICES

For many plans, the development of services and ancillary support elements has frequently been targeted toward the most sophisticated of our participants rather than the least. Unfortunately, while sophisticated participants will utilize the plan and other outside investment opportunities to optimize their retirement preparation, less engaged participants can be overwhelmed by the volume of decisions they are expected to make as participants in a DC plan.

All plan services should be reviewed to determine whether they will help or confuse the core message of retirement readiness and the four factors that impact readiness: contribution rate, investment performance, time horizon, and retirement income needs. Attention should be focused on keeping the plan simple.

Simple to enroll

Simple to use

Simple to allocate

Source: Iyengar, Sheena S.; Jiang, Wei; Huberman, Gur, Pension Design and Structure: New Lessons from Behavioral Finance, "How Much Choice is Too Much?: Contributions to 401(k) Retirement Plans" (Chapter 5). Philadelphia, PA: Pension Research Council, University of Pennsylvania

Each incremental step or question around the plan that does not support simplicity of use may deter the least engaged participants who are most at risk of a successful retirement outcome. That does not mean that additional services are harmful, but the types of financial planning, mutual fund analytic tools, and tax planning tips should not be required elements to the successful use of your retirement plan.

The focus on simplicity has a measurable impact on plan success. One of the most interesting manifestations simplicity offers is with respect to the number of fund options in a defined contribution plan. In a widely cited study, evidence supports that increasing the number of investment options in a retirement plan may decrease the elective plan participation rate.

INVESTMENT STRUCTURES

Investment decisions within the DC arena have historically been focused on selecting the “best” managers. While it is important to identify strong managers, we believe strongly that participants’ retirement readiness can be enhanced through the development of a structured investment menu. We advocate for plan sponsors to evaluate their investment menu and develop a structure that provide participants increasing levels of investment flexibility without sacrificing the simplicity that encourages engagement.

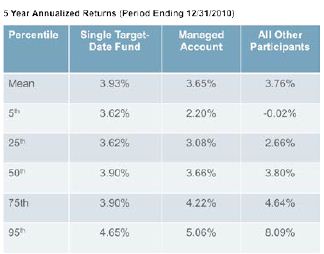

Participants continue to demonstrate an almost uncanny ability to underperform the broader market.

Annualized Returns for the 20 Years Ended 12/31/2010

Source: Dalbar, Inc. 2011 Quantitative Analysis of Investor Behavior

The anemic participant return data continues to fuel the development of new solutions to assist participants in achieving a reasonable return. The two primary "one-stop shops" for investment allocation are managed accounts and target maturity (or target date) products.

Managed Accounts

Managed accounts typically use the core array of underlying products within the plan to create a “customized” asset allocation factoring in information known about the participant. There are a finite number of portfolios a participant may be invested in based on the data known. The benefit of managed account solutions is that they can incorporate significant amounts of data about a participant to develop an allocation. Examples include wages, accumulated retirement savings, outside assets, or spousal income. The use of greater participant information enables a portfolio more refined to a participant’s circumstances. A participant with a low wage and high accumulations may have a more conservative investment allocation than a high wage earner with low accumulations, without regard to their relative ages.

However, the greater flexibility does come with a cost. Managed account solutions generally charge an asset based fee above and beyond the costs of the investment products that participants are allocated to. As a result, a managed account solution should be reviewed to determine the ability to improve retirement readiness in light of the additional services and costs being allocated.

Another limitation of managed account solutions is the requirement for participants to fully engage in order to reap the full rewards that the products offer. For participants willing to commit to provide the full details of financial profile, the managed account can provide a tailored solution. For participants unwilling to commit to engaging fully, the managed account provides little more flexibility than an off-the-shelf portfolio but at a higher cost.

Target Maturity (Target Date)

In most target maturity products, participants are invested in a single "fund" with a pre-determined glide path that becomes more conservative as a participant generally nears a specified age (typically 65). This type of solution provides participants a limited amount of customization using only the date of birth as a required data element. The limited flexibility creates economies of scale that reduce cost compared to managed account products.

While the growth of target maturity products has been significant, they do have limitations. First, while time horizon is an important determinant in developing an investment strategy, it is not the sole factor. Savings rates and income needs are equally important and are not factored into the target date allocation at a participant level. Second, most target maturity products are constructed using proprietary investment products managed by a single investment manager. The use of proprietary funds may cause the target maturity to underperform, as few investment managers have the capabilities to effectively manage assets in all segments of the market. The complexity of these products, with a changing asset allocation and multiple underlying investment strategies, can make it challenging for plan sponsors to assess investment performance and act in accordance with their fiduciary duty.

The selection of appropriate target date investment products can be a challenging one given the broad difference in mandates between managers. For more information on selecting and evaluating target date funds, please reference our white paper, Evaluating Target Date Fund Structure.

The two primary solutions for participant investment delegation, managed accounts and target date funds, each offer pros and cons. Because they tackle the same problem in two different ways, they are not perfect substitutes but rather complimentary tools for plan sponsors to consider. At this point there is no conclusive evidence as to which provides participants the “best” outcome, but what is clear from a recent Vanguard study is that participants who perform poorly in an open architecture investment lineup, do better when supported with the either option.

Source: Vanguard 2011 “Participants During the Financial Crisis: Total Returns 2005-2010”

Core Index

While many participants are overwhelmed by investment selection and account rebalancing, other participants may desire to retain the ultimate control for investing, but still feel uncomfortable selecting investment products. In response to these participants, plan sponsors are constructing core index “tiers” within their investment lineup. These index products provide participants low-cost access to market level returns. Participants can make more manageable decisions about the equity to fixed income allocation for their portfolio, thereby side stepping more granular allocation and manager selection decisions that so few are well-suited to the task.

The focus on default investment alternatives and the roll-out of core index alternatives are not likely to swallow up the participant demand for more extended active investment arrays, mutual fund windows, and brokerage accounts. But in helping drive retirement readiness, emphasis should necessarily be on the needs of those that can be impacted most through menu construction. As with other plan design and structure issues, the most sophisticated of your participant population will drive their own success in accumulating an adequate retirement.

EMPLOYEE EDUCATION

Since the development of the DC plan, sponsors and their retirement plan vendors have been trying to drive more effective employee communication plans that help employees move from novice savers to sophisticated investors. Sponsors have tried group sessions, individual counseling appointments, online training, personalized mailing campaigns and everything short of begging to change participant behavior, and the results have been muted at best.

That is not to say that education does not help. There are countless stories of participants who have learned through the education process and have met with individual counselors to develop custom investment and retirement savings strategies. However, in many cases this portion of the population is in the minority and education resources end up being consumed by the most engaged of your retirement population. A couple of recent reports confirm our experience with education:

"…policy makers should be very concerned that retirement education does not increase the likelihood that financially vulnerable groups – women, persons without a college degree, and particularly persons with lower incomes – will save their distributions."8

Peer behavior may be as or more impactful on participant savings behavior than employee education9

While education may have limited impact to the neediest of your population, it can frequently be an important driver of total plan cost. As a result, sponsors should insist on education that is effective in improving retirement readiness. Participant education is a means to an important end. Education with regard to general financial planning, like with other education resources provided by employers, is best accommodated outside the retirement structure rather than within it. Like with plan design, education should be targeted to speak to the needs of your specific participant audiences: Young Savers, Accumulators, and Pre-Retirees.

Young Savers

Education targeted at Young Savers and new employees should be focused on getting participants enrolled in the plan. Many younger employees lack financial literacy; therefore the education program should be focus on developing a level of financial literacy that will allow them to understand the structure of retirement savings. At this early stage it is important to orient participants to focus on retirement readiness as an income concept and to communicate how their saving and investing patterns impact their retirement readiness.

Participants who seek education on the investment options specifically should have the ability to receive it, but generally the education program for Young Savers should de-emphasize the importance of investment selection in favor of retirement savings. Frequently, plan sponsors use orientation as an opportunity to educate new hires on the retirement plan structure. Plan education is useful, but should not be a requirement or impediment to enrolling and participating in the plan’s benefits.

Accumulators

Providing employees general financial literacy that is appropriate to their life stage will help reduce anxiety and improve decision making for many participants. For Accumulators the range of education topics is likely to expand to healthcare, insurance, social security, etc. The goal is not to create expertise, but to raise awareness.

For Accumulators the power of inertia is strong, so personalized education that reports on the effectiveness of their current savings and investment behavior while identifying specific opportunities to improve retirement readiness can be impactful. At this stage many participants benefit from individual financial counseling as they consider issues related to childcare expenses, mortgage expenses and work through the most complicated period of their financial life. Access to phone, web, and in-person employee education resources can be a helpful bridge to allow participants to improve their retirement readiness.

Pre-Retirees

For most participant education programs in place today the focus is on the needs of Young Savers. Education programs routinely talk about the time-value of money, the importance of beginning to save and the premium that equity investing provides above fixed-income investing. The population with the least at stake is being educated while the population with the greatest accumulated assets and anxiety about savings receives short shrift.

In order for a retirement program to be successful it needs to allow employees to conclude their path in your plan. Education focused on this important and rapidly growing population should be focused on the individual as a whole and less on the plan and its features. Pre-retirees need help understanding how outside assets should be managed, the impact of spousal income on retirement projections, real income needs in retirement, and the sources for retirement income and healthcare benefits. Recently, some providers have begun calculating individual estimates of healthcare cost to assist participants in better understanding their own income needs.

Financial literacy is no longer the primary concern for pre-retirees. This population is looking for specific guidance with regard to asset allocation strategies and the impact of timing on retirement readiness. This type of financial planning is typically best delivered individually and provides pre-retirees an additional opinion as to their retirement preparedness. Plan participants desperately need an accurate assessment of their retirement preparedness in order to give them the comfort to transition to a successful retirement.

Throughout the education process, as with other factors impacting the health of the plan, the focus should be on how these changes improve the likelihood of your population securing a successful retirement.

CONCLUSION

A successful defined contribution plan should be:

Easy to Start – How can your plan reduce any barrier to a participant enrolling and benefiting from your current plan?

Leak-Proof – Plug the holes that allow participants to damage their savings patterns and ultimately lead to longer working careers and higher related employer costs

Safe to Leave – The decision to transition from working to retirement is one of the most complicated decisions many employees will face. Measuring retirement readiness and income replacement from the outset helps participants focus on the correct topics and feel more confident in their decision making process

As with most processes, the best place to start is an assessment of the current health of your plan and the retirement readiness of your population. This type of analysis can help you identify the portions of your population which might benefit from changes in the structure of your plan. From there, continue to take the following path to improving retirement readiness.

Determine Obstacles to New Hire Participation – Enrolling in a retirement plan is too difficult. How much paper must be executed? Is the language focused on the purpose of the plan? How can we speed the process of enrollment?

Develop Mechanisms to Move New Hires Towards Adequate Income Replacement – Automatic escalation is an effective plan design tool, but measuring the impact of changes in asset allocation and savings behavior can also be useful elements in helping participants understand the correlation between their behavior and the success of their retirement savings plan.

Plug the Holes – Saving for an adequate retirement is a career long journey that can be made significantly more challenging when participants leak assets out of their savings during their working years. Holes that cannot be plugged through changes in design should be addressed as part of the education plan.

Build the Communication Plan to Support the Objective – Education plans are typically delivered by the provider but should be based on a strategy established by the sponsor. As education is a major cost component for most service providers, clients should demand objective, measurable results from their education provider. Clients may benefit from developing an Education Policy Statement that focuses on objectives and helps the plan’s vendor develop a custom education strategy that places a tremendous focus on saving for retirement and provides high-touch participant advice and financial planning for pre-retirees.

Each of these process steps can then be measured to determine how retirement readiness is improved. Like nearly all issues related to retirement plan management, driving retirement readiness is a continual process, but one that when well-executed can have a material impact on the financial health of your participants and your organization.

3 Rui Yao and Eric Park, University of Missouri, "Do Market Returns Affect Retirement Timing?" 2011

4 Rui Yao and Eric Park, University of Missouri, "Do Market Returns Affect Retirement Timing?" 2011 5 U.S. Department of Health and Human Services, "National Health Care Expenditure Sheet." Data as of 2004

† Information contained herein is provided “as is” for general informational purposes only and is not intended to be completely comprehensive regarding the particular subject matter. While Multnomah Group takes pride in providing accurate and up to date information, we do not represent, guarantee, or provide any warranties (express or implied) regarding the completeness, accuracy, or currency of information or its suitability for any particular purpose. Receipt of information herein does not create an adviser-client relationship between Multnomah Group and you. Neither Multnomah Group nor any of our advisory affiliates provide tax or legal advice or opinions. You should consult with your own tax or legal adviser for advice about your specific situation.